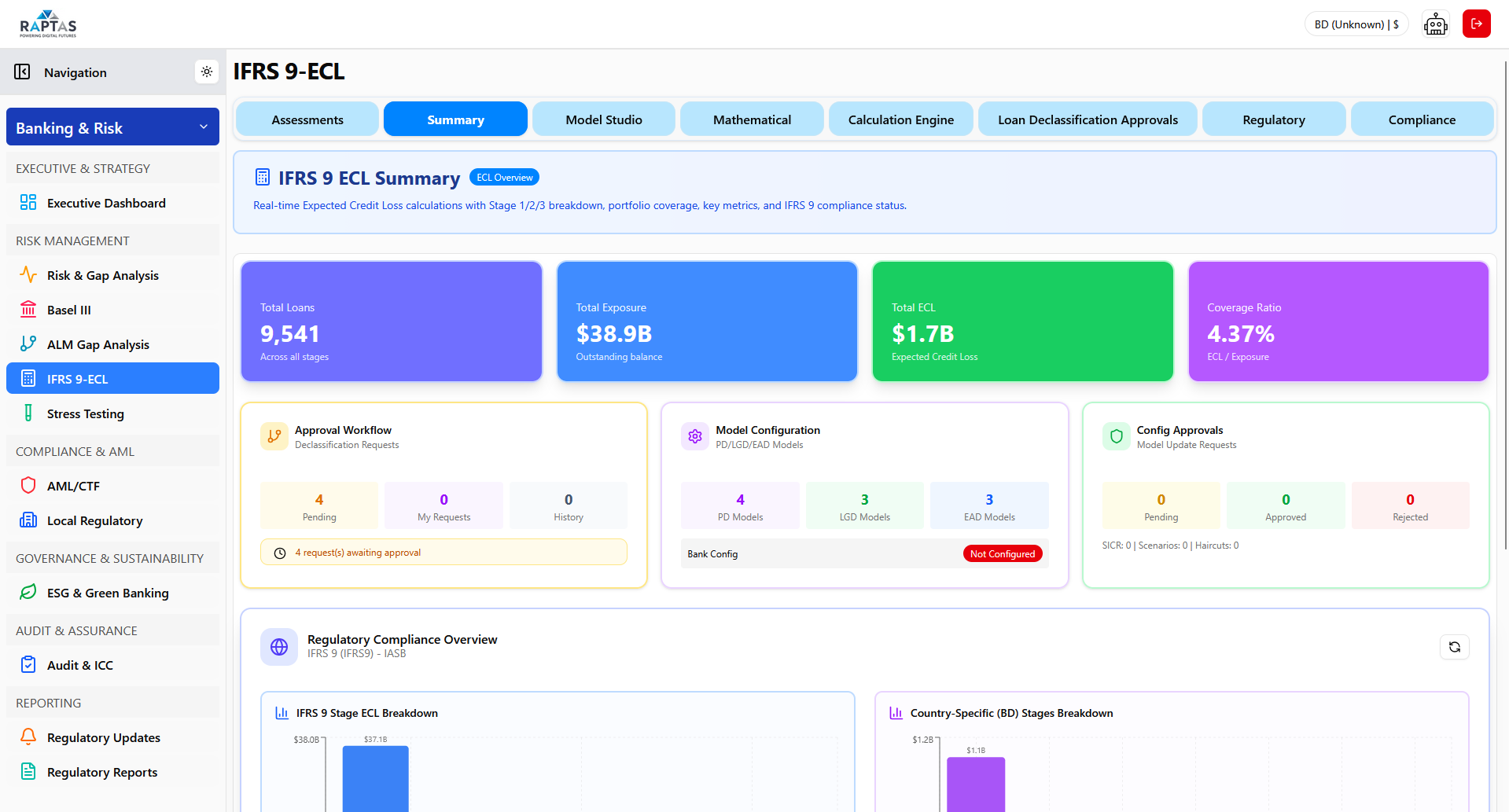

The Shift from Incurred to Expected Loss

IFRS 9 fundamentally changed how banks recognize credit losses. Instead of waiting for losses to occur (the old IAS 39 approach), banks must now predict and provision for expected losses from day one.

This forward-looking approach affects over 140 countries and impacts trillions in global banking provisions.

The ECL Formula: Simple Yet Powerful

At its core, Expected Credit Loss is calculated using three risk parameters:

The real complexity lies in how these parameters are estimated—especially for banks without sophisticated internal models.

The Three-Stage Model

IFRS 9 classifies every financial asset into one of three stages based on credit quality changes:

| Stage | Status | ECL Horizon | Trigger |

|---|---|---|---|

| Stage 1 | Performing | 12-month losses | No credit deterioration |

| Stage 2 | Watch | Lifetime losses | Significant Increase in Credit Risk (SICR) |

| Stage 3 | Impaired | Lifetime losses | Default occurred |

Key Point: Moving from Stage 1 to Stage 2 can dramatically increase provisions because the ECL horizon jumps from 12 months to the full remaining life of the loan.

What Triggers Stage Migration?

Banks evaluate 22 indicators to determine if credit risk has increased significantly:

| Quantitative Triggers (Auto-SICR) | Qualitative Triggers |

|---|---|

| - Days past due > 30 days | - Forbearance or restructuring granted |

| - PD increase > 100% from origination | - Watchlist placement |

| - Rating downgrade > 3 notches | - Adverse industry conditions |

| - DSCR falls below 1.10 | - Management or ownership changes |

| - Covenant breach |

Best Practice: Any single auto-SICR trigger moves the asset to Stage 2. For qualitative indicators, two or more triggers typically warrant stage migration.

The Three Risk Parameters Explained

1. Probability of Default (PD)

What it measures: The likelihood a borrower will default

Two flavors:

- Point-in-Time (PIT): Reflects current economic conditions (preferred for IFRS 9)

- Through-the-Cycle (TTC): Long-term average (used for Basel capital)

How it's derived:

- Credit scoring models (behavioral + financial factors)

- Historical default rates by rating grade

- External agency ratings mapped to PD

Example PD by Rating:

| Rating | 12-Month PD | 5-Year Cumulative PD |

|---|---|---|

| AAA | 0.02% | 0.10% |

| BBB | 0.30% | 1.50% |

| BB | 1.50% | 7.50% |

| CCC | 25.00% | 50.00% |

2. Loss Given Default (LGD)

What it measures: The percentage of exposure lost after recoveries

Key components:

- Collateral value (after haircuts and time to realize)

- Recovery from guarantees

- Unsecured portion recovery

- Workout costs and time value

Typical LGD ranges:

| Collateral Type | Normal LGD | Stressed LGD |

|---|---|---|

| Cash/Deposits | 0-5% | 5-10% |

| Residential Property | 15-25% | 30-45% |

| Commercial Property | 25-40% | 45-65% |

| Unsecured Corporate | 40-50% | 55-70% |

| Unsecured Retail | 60-75% | 75-90% |

3. Exposure at Default (EAD)

What it measures: Total amount exposed when default occurs

Varies by product:

| Product | EAD Formula |

|---|---|

| Term Loan | Outstanding principal + accrued interest |

| Revolving/OD | Drawn + (Undrawn × CCF) |

| Letter of Credit | Face value × CCF |

| Derivatives | Current Exposure + PFE − CVA + DVA |

Credit Conversion Factor (CCF): Estimates how much of undrawn limits will be drawn before default. Typically 50-75% for corporate revolvers, 80-95% for retail cards.

Scenario-Based ECL: The Forward-Looking Requirement

IFRS 9 mandates incorporating forward-looking information through multiple economic scenarios:

Macro variables driving scenarios:

- GDP growth rate

- Unemployment rate

- Interest rates

- Property price indices

- Industry-specific indicators

Global Framework Comparison

| Aspect | IFRS 9 | US CECL | Basel IRB |

|---|---|---|---|

| Adoption | 140+ countries | USA only | Global (capital) |

| ECL Horizon | 12M or Lifetime | Always Lifetime | 1 year |

| Staging | 3 stages | None | N/A |

| PD Type | Point-in-Time | Lifetime | Through-the-Cycle |

| Scenarios | Probability-weighted | Probability-weighted | Single estimate |

Local overlays: Many jurisdictions add requirements on top of IFRS 9—UAE's 5-category system, Bangladesh's 7-stage classification, India's NPA norms, ECB's enhanced disclosures.

Derivatives: The CVA/DVA Adjustment

For derivative exposures, banks must account for counterparty credit risk:

- Fair Value = Risk-Free Value − CVA + DVA

- CVA = Expected loss from counterparty default

- DVA = Expected gain from own potential default

- For ECL: Derivative ECL ≈ CVA

Individual vs. Collective Assessment

| Approach | When to Use | Method |

|---|---|---|

| Individual | Large corporates, significant exposures | Full account-level analysis with specific PD/LGD |

| Collective | Retail portfolios, homogeneous pools | Statistical models applied to segments |

Most banks use both: individual for top exposures, collective for volume portfolios.

Implementation Best Practices

✅ Data-Driven Calibration Derive risk parameters from your own historical data, not generic assumptions

✅ Configurable Framework Build flexibility for changing regulations and jurisdiction-specific rules

✅ Hybrid Modeling Combine statistical scores with expert judgment—no single model fits all

✅ Complete Audit Trail Document every decision, override, and parameter change

✅ Regular Backtesting Compare predictions to actuals; recalibrate when performance drifts

Key Takeaways

-

ECL = PD × LGD × EAD — simple formula, complex estimation

-

Three stages determine whether you provision for 12 months or lifetime

-

SICR triggers (22 indicators) drive stage migration—get this right

-

Forward-looking scenarios are mandatory, not optional

-

Calibration to your portfolio is essential for accuracy and regulatory acceptance

-

Local requirements layer on top of core IFRS 9—know your jurisdiction

The Bottom Line

IFRS 9 ECL assessment isn't just compliance—it's a lens into your portfolio's true credit risk. Banks that master it gain:

- Earlier warning of credit deterioration

- More accurate provision levels

- Better capital planning through stress scenarios

- Regulatory confidence in their risk management

The banks that treat ECL as a strategic capability—not just a reporting burden—will be better positioned to navigate credit cycles and regulatory scrutiny alike.

Ready to transform your ECL process? Contact us to learn how GRC Sphere helps banks achieve IFRS 9 compliance with confidence.